Leasehold vs Freehold Property: A Global Perspective on Smarter Investment Decisions

Understanding the Core Differences

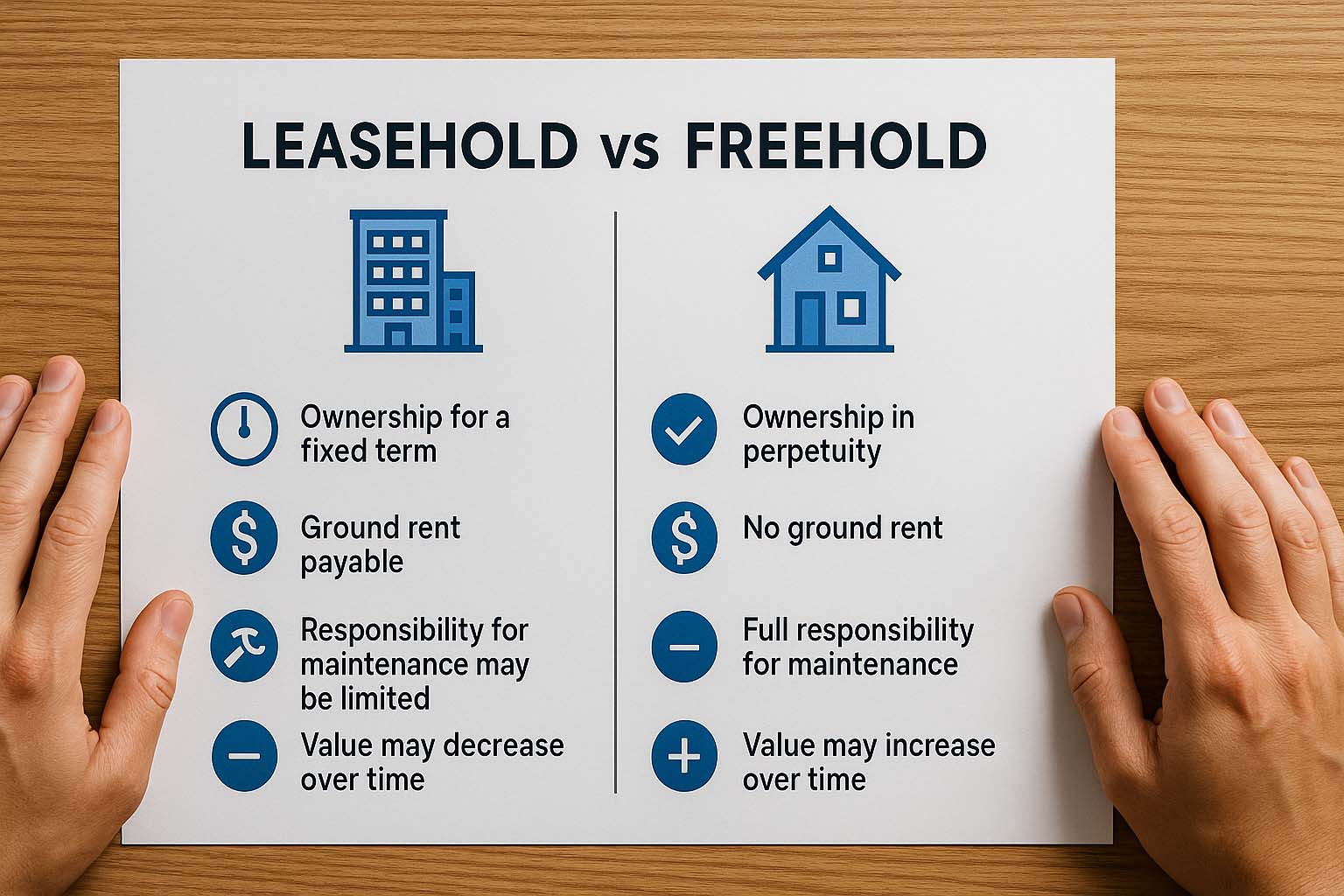

In making long-term wealth decisions, choosing the type of property ownership is one of the most critical steps. Leasehold and freehold are two common forms available to buyers across the world. Both lead to ownership in some form, but the duration, control, and financial obligations differ greatly. Whether you’re an individual buyer, a cross-border investor, or part of a financial advisory team, knowing these distinctions will shape your expectations and financial returns.

- Leasehold: Ownership is time-bound—often between 30 to 99 years. When the term expires, the property typically reverts to the landowner unless a new agreement is made.

- Freehold: Full ownership of land and structure with no expiry.

- Impacts resale value, mortgage approval, and long-term earnings.

Historical Roots of Property Titles

The roots of leasehold and freehold arrangements trace back to feudal Europe. Monarchs granted land to nobles or religious orders in exchange for taxes and loyalty. Over time, legal systems evolved to formalize these arrangements. In high-density cities like London, Hong Kong, and Dubai, leasehold became widespread due to limited land. In contrast, suburban growth in places like the United States, Australia, and parts of Europe leaned toward freehold to attract families seeking long-term stability.

Investor Considerations Across Countries

Before diving into international property markets, consider the following:

Land ownership laws: Some governments allow foreigners to fully own land, while others require a local partner to lease or co-own.

Lease duration: Properties with longer lease terms retain value better. Once the remaining lease drops below 20 years, it becomes harder to sell and finance.

Bank preferences: Many lenders favor freehold properties. Loans for leaseholds with fewer than 40 years remaining are rarely approved.

Benefits and Drawbacks of Both Options

- Leasehold — Advantages

- Lower upfront cost, making it ideal for first-time buyers.

- Many urban developments use leasehold titles, offering central locations.

- Annual charges may be capped or fixed, offering predictability.

- Some responsibilities, such as major repairs, may fall on the landowner.

- Leasehold — Disadvantages

- Depreciating value as the lease term shortens.

- Recurring ground rent and service charges may increase over time.

- Major renovations often require permission from the landowner.

- No ownership beyond the lease term unless it is renewed.

- Freehold — Advantages

- Full control over land and building decisions.

- Easier to transfer through inheritance or resale.

- Greater loan approval chances with higher value ratios.

- No ground rent obligations, just local property taxes.

- Freehold — Disadvantages

- Higher purchase prices, especially in city centers.

- All maintenance costs fall on the owner.

- Some countries restrict foreign freehold ownership.

- Property taxes may be higher due to permanent ownership rights.

Financial Outcomes and Cost Implications

Initial savings may come with a leasehold title, but long-term analysis can be complicated. For example, a Swiss national purchases a 40-year leasehold apartment in Sydney. While the price is attractive today, resale becomes a problem once only 20 years remain. Most banks won’t finance it, reducing the buyer pool and forcing a price drop or reliance on increasing annual costs, like ground rent.

In another case, a Berlin-based entrepreneur invests in a freehold duplex. Although his mortgage is larger, the lack of a lease expiry allows flexible use—from long-term rentals to seasonal platforms. If nearby infrastructure boosts property value, all gains go directly to him.

Bank and Financial Institution Preferences

Lenders often consider two main points:

Loan vs Lease Duration: Loans must not exceed the remaining lease years. A 30-year loan typically requires at least 50 years left on the lease.

Collateral Confidence: Banks are more open to freehold-backed loans, knowing the resale market is broader.

Another concern is insurance. Premiums are often lower for freehold titles because there are fewer maintenance conditions compared to leasehold contracts. Leaseholds sometimes involve obligations that increase risk for insurers.

Legal Commitments of Ownership

Leaseholders agree to a list of conditions written into the lease, often covering repairs or upkeep of certain parts like the roof or garden. Violating these terms can lead to penalties or even termination of the lease. Freeholders, meanwhile, set their own internal rules. While that means more autonomy, it also brings full financial accountability if major repairs arise.

Real-World Applications by Country

United Kingdom: Central London properties often come with 99 or 125-year leases. Market depreciation becomes noticeable when less than 80 years remain. Once it dips below 70 years, owners must pay a fee called “marriage value” to extend the lease.

Singapore: Many upscale condominiums operate on 99-year leaseholds. Once the term falls below 60 years, banks start reducing valuation. On the other hand, freehold landed homes remain highly sought-after, even in outer districts, due to limited availability.

United States: Most suburban single-family homes are freehold, also referred to as fee simple. However, select areas in Hawaii use leasehold systems, typically for 55 years, under royal estate arrangements.

United Arab Emirates: Certain emirates allow foreigners to hold 99-year leases. Full ownership, though, is restricted to specific freehold zones designated by the government.

Questions to Ask Before You Commit

To choose wisely, reflect on the following:

How long do you plan to use or keep the property? If short-term, leasehold may be practical. For lifetime use, freehold gives more security.

Do you plan to use it as collateral or pass it down? Freehold gives more options for succession and financing.

What legal conditions are tied to the title? Read lease agreements carefully. Check who handles major repairs and how fast costs like ground rent rise.

What’s the local lender’s stance? Always speak with a bank before making commitments. Financing terms often hinge on the title type.

Making a Calculated Choice

Deciding between leasehold and freehold isn’t simply about money. It reflects your long-term vision, how much risk you’re willing to take, and how long you intend to hold on to the asset. If living close to the urban center matters most and you’re comfortable with a finite term, leasehold might work for you. If you prefer long-term ownership and greater flexibility in how the property is used or passed on, then freehold fits better.

Before signing anything, examine the contract closely, run the numbers carefully, and confirm local regulations. The more you clarify early on, the better your chances of building lasting value through your property decisions.